Two of my most prized possessions (aside from my custom-made G&L Telecaster) are personally autographed copies of two classic works by Michael E. Porter – you know the guy from the Harvard B-School that keeps telling BAI attendees that most banks have no clear competitive strategy. The comment is equally relevant to our credit union friends. I trust that Mike will let us borrow a classic model of his to illustrate a critical issue for all financial services providers – you have to stay away from the Black Hole of strategy. Take a look.

Click image to enlarge

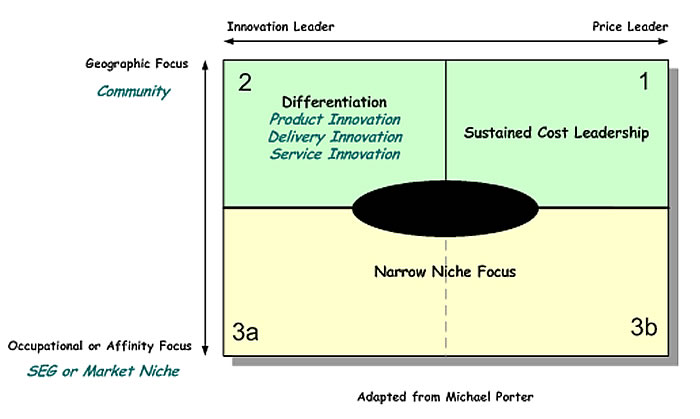

This is a model from Porter’s 1980 classic, Competitive Strategy. I have made a few alterations to fit the financial services industry. After all the management books written, Porter is still right in proposing that there are only three viable operating strategies for any business. The horizontal axis ranges from innovation to price leadership. The vertical axis ranges from very narrow niche customer focus to everyone and their Aunt Suzie. To simplify, the horizontal axis represents “how” and the vertical represents “who.” How many CEOs do you know (be they bank, thrift or credit union) that can quickly tell you the “who” and “how” of their strategy without hesitation – or without making it up on the spot? How many bank strategies today really articulate what the bank will not be?

It is easy to spot the organizations that have this figured out. The current tough times notwithstanding, they demonstrate enviable revenue growth. They have a clear directional focus.

Click image to enlarge

Take a look at the institutions that have been able to keep a tight lid on their operating costs (Basic strategy No. 1). Their characteristics include:

Financial institutions can be spotted all over the map that have turned strict cost control into competitive advantage. They have the flexibility to use price as a weapon when opportunities arise. The rest of us rationalize that our value proposition is based on service or convenience, but without a clear differentiation, we end up wasting resources that cost leaders avoid.

But that’s not the only viable strategy. Area number 2 is characterized by innovation. The industry press is full of stories of financial institutions, large and small, doing exciting things in pursuit of innovation.

Caveat: Successful innovators cannot thrive without good cost-benefit analysis and expense control mechanisms. There are too many great new ideas – too many new technologies. All capital investments have to be thoroughly vetted and aligned with strategic objectives.

The bottom half of the model illustrates the classic niche strategy. The 3a side of the bottom half of the model is a blend of a well defined customer focus mixed with innovation that meets well defined customer needs – a powerful combination in any industry.

The 3b side represents the more traditional provider that has been able to resist the siren call to expand beyond their reach. Traditional credit unions that have continued to serve one, or a few, large employee groups and have also kept their costs to a minimum continue to thrive. They continue to deliver significant economic benefit and build deep relationships based on affinity – an equally powerful combination.

The truth is that there is success to be had on every corner of this model. The farther from the center you can get, the better chance you have of creating real and lasting customer value and sustaining growth. Unfortunately, the trip from the middle to the outer limits is easier on the innovation side. Once operating expenses have moved beyond the peer average, it is very difficult to move them back without a lot of pain.

The most common characteristic of financials that operate toward the outer edges of the model is that they know who they are serving and how best to get the job done. They consistently focus their efforts knowing what their customers want and need. The often have formal research and development functions, consistently matching new products and technologies to well understood customer segments.

The Black Hole

Let’s talk about the majority of banks that find their organizations struggling at the center of this model – the area we call “The Black Hole.” Many financial institutions have drifted into the center over time. Credit unions, for example, started out with great sponsor support. Most did very well in the 1980s and 1990s. A rising tide does indeed raise all ships. But with the consistent loss of sponsor support over the past 20 years, and the rush to move into uncharted community waters, they just got lost – or did only well enough to maintain the status quo. GonzoBankers can see all the wreckage of others and usually manage to avoid the pitfalls, but many ship captains out there are still wandering, looking for a new heading with a broken compass. There are a number of common characteristics here.

Why do so many institutions find themselves in the Black Hole? Here are a few thoughts:

It may seem counterintuitive, or even silly to be thinking about strategic direction staring down one of the worst potential economic years in a long time. We all have a lot to think about. But we believe 2008 is the perfect time to start paddling in a new direction. There are several good reasons.

As we head into a time of great fear and anxiety in the financial markets, banks and credit unions certainly need to “buckle down” and get their financial houses in order. At the same time, only those competitors that keep their eye on long-term strategy will come out of this darkness as the growing, entrepreneurial leaders of our next prosperous times. Why not be Gonzo and try to be one of these leaders?

-tt